On the morning of April 7th, with the stock market reeling, I issued a special message to clients, noting that the pace at which the market had fallen had not been seen since the Covid-19 panic.

I quoted Vanguard Founder John C. Bogle who famously said that “Time is your friend; impulse is your enemy and reminded our clients that “Periods of panic can present opportunities for disciplined, long-term investors”.

On that day, the S&P 500 reached an intraday low of 4,835. At the close of the second quarter, the S&P 500 closed at 6,205, with a gain of 1,360 points or 28%. Traders on Wall St., call that a monster truck rally!

Looking back, I observe that the second quarter of 2025 showcased both the resilience of financial markets and their sensitivity to policy uncertainty. From the White House’s tariff announcements in April to escalating tensions between Israel and Iran in June, investors faced many challenges. Yet, the stock market went on to stage one of the fastest rebounds in history and finished the quarter at new all-time highs.

Overall, it was a strong quarter for stocks, while bonds also delivered positive outcomes. For long-term investors, these events are a reminder that while headlines can drive short-term swings, maintaining perspective and staying focused on fundamental trends remains the key to achieving financial goals.

Key Market and Economic Drivers in Q2

The S&P 500 and the Nasdaq both ended the quarter at record highs, gaining 10.6% and 17.7% over the three months, respectively. The Dow Jones Industrial Average rose 5.0% and is 2% below its record level.

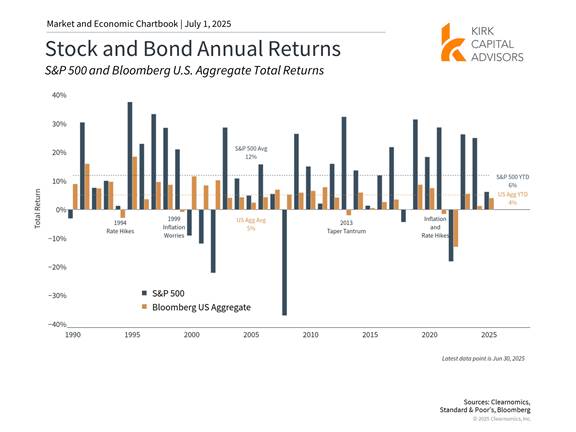

The Bloomberg U.S. Aggregate Bond Index gained 1.2% in the second quarter. The 10-year Treasury yield ended the quarter at 4.2% after reaching as high as 4.6% in May.

Developed market international stocks (MSCI EAFE) rose 10.6% and emerging market stocks (MSCI EM) increased 11.0% in the quarter.

Gold rallied to a new record level of $3,431 per ounce, before settling at $3,308 to end the quarter.

Bitcoin reached a high of $111,092 in May and hovered around $107,000 at the end of June.

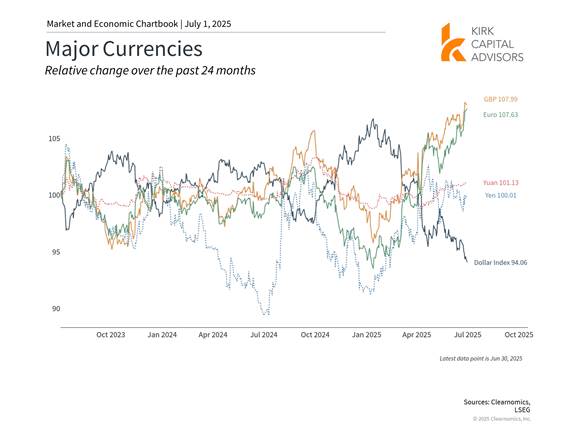

The U.S. Dollar Index continued to fall over the quarter, ending the quarter at 96.88. It started the year at 108.49.

The Consumer Price Index rose 2.4% year-over-year in May, while core inflation, which excludes food and energy, came in at 2.8%.

The University of Michigan Consumer Sentiment Index improved in May to 60.7, its first increase in six months. Consumers expect an inflation rate of 5.0% over the next year, down from 6.6% in the previous survey.

At its June meeting, the Federal Reserve kept rates unchanged within a range of 4.25 to 4.5%.

Markets rebounded to new all-time highs

Despite significant volatility, the stock market recovered quickly once the worst-case scenarios for tariffs and geopolitical tensions did not materialize. The quarter began with heightened uncertainty following the announcement of new tariffs on April 2, which were more far-reaching than many investors had anticipated.

However, as the administration engaged in negotiations and reached preliminary trade agreements with several partners, market sentiment improved. The Middle East conflict created a similar outcome, although markets were broadly resilient and went on to new highs after the ceasefire between Israel and Iran was announced.

The equity market rebound was widespread, with many sectors, styles, and regions delivering positive outcomes. International stocks continue to lead the way in 2025, especially with the dollar weakening. Small cap stocks have lagged other parts of the market due to their greater sensitivity to tariffs and domestic trends, and the Russell 2000 index is still down -2.5% this year.

At a sector level within the S&P 500, Information Technology stocks experienced a strong recovery and contributed toward the new market highs. Many other sectors are supporting markets too, including Industrials which are now up 11.4% on the year, Communications which have gained 10.2%, and Financials up 7.5%. On the other end, Healthcare and Energy saw weakness.

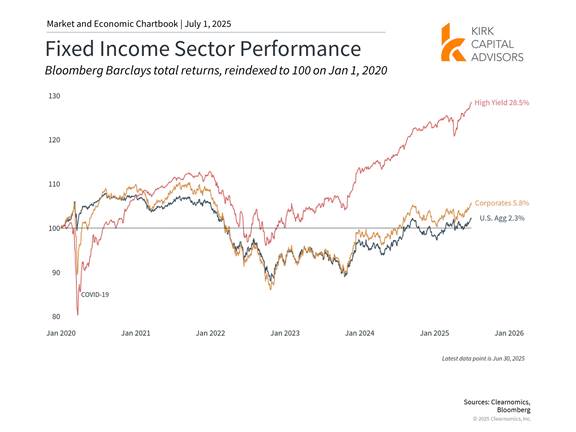

Bond markets are also quietly contributing to portfolio outcomes, with relatively strong yields and falling credit spreads contributing in the quarter. Treasury securities and corporate bonds also experienced volatility during the tariff-induced drawdown, although the quarter ended in positive territory.

The dollar continued to weaken

The U.S. dollar weakened through the second quarter despite tariff pressures. While a weaker dollar can be negative for consumers, it can be positive for U.S. businesses and exporters, since it becomes cheaper for those using foreign currencies to buy our goods. While the dollar has declined this year and is near the low end of its range since 2022, its value is still high compared to the past decade.

When it comes to monetary policy, the Federal Reserve held interest rates steady at 4.25% to 4.5% throughout the quarter, reflecting a measured approach to monetary policy in an evolving economic environment. Fed Chair Jerome Powell emphasized the Fed’s focus on price stability even as other factors complicate the economic outlook.

Specifically, the Fed’s updated economic projections reveal the challenges policymakers face. Officials now expect inflation to reach 3% in 2025 before moderating to 2.1% by 2027, marking an upward revision from earlier forecasts. They also expect real GDP growth to slow this year to 1.4%, a downgrade from a 1.7% projection in March. These adjustments reflect concerns that tariffs could spur inflation and slow growth.

The conflict between Israel and Iran added another layer of complexity to an already challenging environment. Israeli strikes on Iranian nuclear facilities and military targets beginning June 13 created immediate concerns about regional stability and potential escalation. However, the two countries agreed to a ceasefire after 12 days of fighting.

Bonds helped to provide portfolio balance

While the stock market has ended the quarter at new all-time highs, the decline and rebound was challenging for many investors. Fortunately, bonds helped to support balanced portfolios during the quarter. High yield, corporate, and Treasury bonds all provided balance and are positive year-to-date. Interest rates have remained higher than many had expected, and short-lived concerns in April about a flight from U.S. Treasury securities did not occur.

Budget discussions in Washington have brought renewed attention to America’s fiscal trajectory. The national debt now exceeds $36 trillion, or approximately $106,000 per American. According to the Congressional Budget Office, the latest budget proposal could add an estimated $3.3 trillion in deficits over the next decade. While the proposal includes spending reductions, these are outweighed by tax cuts and spending increases elsewhere.

Moody’s downgraded the U.S. credit rating in May, citing concerns about successive administrations and Congress failing to address “large annual fiscal deficits and growing interest costs.” This echoes similar challenges raised during previous budget standoffs in 2011, 2013, and from 2018 to 2019. However, in each instance, agreements were eventually reached, markets stabilized, and economic growth resumed.

For long-term investors, these fiscal debates underscore the importance of maintaining diversified portfolios that can weather various policy outcomes. While deficit levels deserve attention, history suggests that the U.S. economy’s fundamental strengths and adaptability remain intact.

The bottom line? The second quarter demonstrated both market volatility and resilience as investors navigated policy changes and global tensions. For investors, maintaining perspective and focusing on asset allocation strategies remain the most effective way to achieve long-term goals.

This newsletter is a publication of Kirk Capital Advisors, LLC. It should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. A professional advisor should be consulted before any investment decisions are made. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for your investment portfolio. All investment strategies have the potential for profit or loss. Historical performance results for investment indexes and/or categories, generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment management fee, the incurrence of which would have the effect of decreasing historical performance results. Kirk Capital Advisors, LLC is registered as an investment advisor and only transacts business in states where it is properly registered or excluded or exempted from registration requirements. Registration as an investment advisor does not constitute an endorsement of the firm by securities regulators nor does it indicate that the advisor has attained a particular level of skill or ability. ©2025 Kirk Capital Advisors, LLC.

Copyright (c) 2025 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security–including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.